Getting ready for CSRD

Comprehensive ESG Assurance: Elevate Your Sustainability Reporting with TÜV Rheinland

As an independent third party with a strong background and knowledge of ESG issues, TÜV Rheinland can provide assurance services for your sustainability and ESG reports.

In line with the EU Green Deal, the new EU Corporate Sustainability Reporting Directive (CSRD) introduces a significant expansion of environmental, social and governance (ESG) reporting requirements.

The CSRD must be transposed into national law in all member states within 18 months, by July 6, 2024. This must be done in such a way that the Directive can be applied as of January 1, 2024, meaning that it may have to be implemented retroactively.

CSRD aims to strengthen sustainability reporting to stakeholders and to improve the disclosure of non-financial information by companies − meaning everything they do voluntarily and without financial motivation for the sustainability of their company. Which companies are affected depends on several criteria.

The CSRD also requires companies to obtain limited assurance on the sustainability information they disclose. This assurance must be provided by an impartial, reliable, and experienced third party engaged to verify the data.

Contact us now and our experts will support you in meeting the CSRD requirements!

What is CSRD About?

Central to the CSRD is the inclusion of sustainability statements in the company's annual report. These statements should include a mix of sector-agnostic, sector-specific, and company-specific information that is closely aligned with the requirements of the European Sustainability Reporting Standards (ESRS).

The CSRD will effectively replace the Non-Financial Reporting Directive (NFRD) and significantly expand both the reporting obligations and the scope of companies that will be required to report.

In addition, the CSRD includes the formulation of implementation plans to facilitate the transition to a sustainable economy.

Companies will need to provide insight into the due diligence processes used to address sustainability issues and outline the actual and potential negative impacts of their operations and value chain.

TÜV Rheinland's ESG team is ready to support companies of all sizes comply with the CSRD:

- Sustainability strategy and goal setting

- Materiality assessment

- Pre-assurance and CSRD readiness assessment

- Stakeholder engagement and capacity building on key topics

- Assurance services conducted by a verification team independent from advisory services

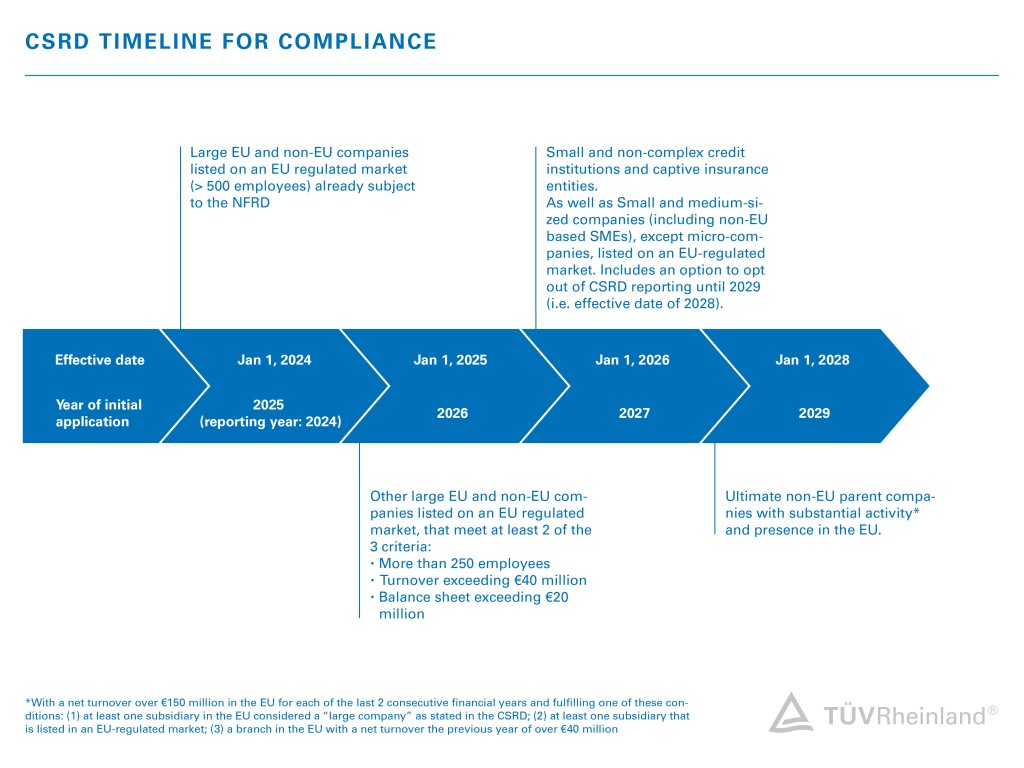

To Whom and When is CSRD Mandatory?

Understanding the CSRD timeline is crucial for companies of different sizes and with different reporting requirements:

How to Fulfill CSRD

1. Materiality Assessment

2. Strategy Planning and Target Setting

3. Measurement and Data Collection

4. Transparent Sustainability Reporting

5. Sustainability Report Assurance

One of the key differences between the CSRD and the current ESG reporting practice is the requirement for a materiality assessment based on the double materiality concept. This requires companies to examine the sustainability issues that affect them, while also assessing their impact on broader sustainability issues.

It is critical to first understand which issues are relevant to your business and how your business is affected by them. It's important to ensure that all stakeholders and value chain partners at different levels are involved in the assessment process. Consider the short-, medium-, and long-term impacts of your business.

Materiality assessment is a complex process which can be time and resource consuming. Companies are encouraged to start the process as early as possible to ensure the preparedness for CSRD reporting.

TÜV Rheinland supports meeting all requirements of CSRD.

Based on the outcome of the materiality assessment and alignment with UN Sustainable Development Goals (SDG) as well as other applicable sector and country sustainability targets, companies should develop an impactful and forward-looking overarching sustainability strategy with milestone targets.

TÜV Rheinland supports the fulfillment of all requirements of the CSRD.

A clear measurement and reporting methodoloy should be implemented to ensure effective progress tracking and year-over-year data disclosure. This includes KPIs such as greenhouse gas (GHG) calculation and its related emission scopes.

Under the CSRD, the ESG information and data should be included from own business operations, supply chain , and business partners.

More information is offered by our sustainable carbon service , which can be found in the related services section.

TÜV Rheinland supports meeting all requirements of CSRD.

For CSRD reporting, companies should report their overall sustainability performance based on the ESRS standards in a digital format. It is important to have a deep understanding of the ESRS standards and guidelines to ensure effective reporting and minimize gaps.

TÜV Rheinland supports meeting all requirements of CSRD.

The CSRD requires companies to seek independent third party verification for their reporting, starting with a limited level of assurance and gradually transitioning to reasonable level at a later stage. The outcome of the assurance engagement will provide objective opinions from third party assurance practitioners and set a baseline for companies to continuously improving their ESG disclosure process and information quality.

TÜV Rheinland supports meeting all requirements of CSRD.

How TÜV Rheinland Can Assist You in Fulfilling CSRD Requirements

We can assist you with all five steps of the CSRD.

Our assurance services include a comprehensive assessment of key performance indicators (KPIs) and selected sections or the entirety of your sustainability report, providing either limited or reasonable assurance, depending on your needs.

By a verification team independent from advisory services, we create an assurance statement suitable for publication in your sustainability report. It reflects our independent review and validation of the information disclosed.

In addition, we provide a detailed internal management report that highlights key strengths and weaknesses in the underlying processes to facilitate future improvement initiatives. We can help you improve stakeholder engagement and build capacity on key issues.

Our assessment also includes an evaluation of adherence with relevant reporting standards and guidelines to ensure alignment with industry best practices.

FAQ

Show all

Hide all

More about ESG

Contact